Thank you for your choosing us as your Servicer. This Merchant Operating Guide contains simple, easy to-read instructions for processing card transactions with us and minimizing the risk of fraud to your business.

This guide is a part of the Agreement with us. Please familiarize yourself with this guide as you are the first line of defense against fraud. Failure to comply with these guidelines and suggestions may be considered a breach of the Agreement and may result in financial loss to your business. In the event that compliance with this Merchant Operating Guide would cause you to violate applicable Payment Network Regulations and/or Laws, you should comply with such applicable Payment Network Regulations and/or Laws.

Throughout this guide terms that have specific meaning to the Card industry are noted with initially capitalized letters (e.g., Credit Card, Card Present Transactions).

Types of Cards include:

To accept Credit Cards, Debit Cards or other Cards for payment, you process the Transactions through a POS Device and/or with point-of-sale software. A group of Transactions is called a Batch, and the process of sending these Transactions to us is called Settlement.

When you settle a Batch, information for each Transaction is sent to clearing networks across the country and sometimes around the world. Based on each Card number, we send information about a Transaction to the corresponding Issuer so they can charge the Cardholder. Then, funds for the Transaction are deposited into your Demand Deposit Account (DDA). Refer to Chapter 2, Processing Transactions, for specific details about processing Transactions.

In exchange for these services, you are charged a percentage of each Transaction (known as a Discount), along with Transaction fees, Authorization fees, and any other fees specified in the Agreement. Fees are deducted from your DDA on either a monthly or a daily basis.

When a Cardholder does not agree with a Transaction posted to his or her account, the Cardholder can contact the Issuer and initiate a dispute. In this case, the Transaction amount is debited from your DDA and we send you a Chargeback notice. In order to protect your rights, it is important that you respond promptly to any Chargeback notice you receive. Refer to Chapter 6, Retrieval Requests & Chargebacks, for a detailed explanation of this process.

When you process Transactions, it is important to keep the following general guidelines in mind:

In addition to the traditional Card processing services offered, we also provide the following services:

Please contact us if you are interested in any of these services.

This Chapter explains the two steps involved in the Transaction process—Authorization and Settlement— as well as the different types of Transactions.

The first step in processing a Transaction is to request Authorization from the Issuer to accept a Card for payment. Merchant must obtain an Authorization Code before completing any Transaction. An Authorization request is made via one of the following two methods:

Most Authorizations are requested electronically. Voice Authorization is usually used if a Merchant does not have a working POS Device or if the Issuer requests additional information during Electronic Authorization.

An Authorization request is required for every Transaction to determine if:

Receipt of an Approval Code in response to an Authorization request does not:

Merchant will follow any instructions received during Authorization. Upon receipt of an Authorization Code, Merchant may consummate only the Transaction authorized and must note the Authorization Code on the Transaction Receipt. In any case in which a Transaction is completed without imprinting the Card, the Merchant, whether or not an Authorization Code is obtained, shall be deemed to warrant the true identity of the Customer as the Cardholder.

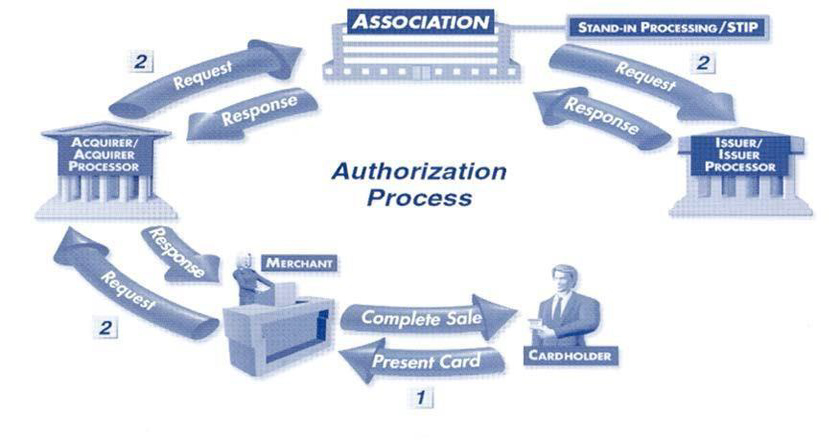

The following diagram describes the Electronic Authorization process:

Figure 2-1. Authorization Process

1. Authorization of Purchase: The Transaction process begins when a Cardholder wants to buy goods or services using a Card. Before the Transaction can be completed, the Merchant must receive an Approval Code from the Issuer.

2. Servicer Host: The Merchant’s POS Device sends the Transaction data to the Servicer Host to verify the MID, to read the Card number, and to route the information to the appropriate Issuer.

3. Issuer: The Servicer Host sends the information to the Issuer through the Discover Network, Visa, or MasterCard network, or directly to other Issuer networks (e.g., American Express). The Issuer determines whether the Transaction should be approved and sends one of the following responses back to the Servicer, who then forwards it to the Merchant:

Exception Processing

ATTN: Card Pick Up

Allegiance Merchant Services

1401 Central Avenue

Charlotte, NC 28205

4. Servicer Host: The Servicer Host receives the response from the Issuer and routes it to the Merchant.

5. Merchant: The Merchant receives the Issuer’s response from the Servicer Host and follows the appropriate steps to complete the Transaction.

For any approved amount received pursuant to an Authorization request that will not be included in a Transaction presentment for Settlement, a full or partial authorization reversal must be processed by the Merchant:

This requirement does not apply if the Merchant is properly identified with any one of the following MCCs:

The final step in processing a Transaction is Settlement, which occurs when the Merchant sends all of its Card Transactions to Servicer to receive payment. During Settlement, the Merchant is paid and Cardholders are billed for previously-approved Transactions.

NOTE: This process can take two or more business days (excluding holidays) unless you are set up for delayed funding.

The following diagram describes the Settlement process:

1. Merchant: Sends all approved, un-settled Transactions (known as the open Batch) in the POS Device to the Servicer Host to close or settle the Batch.

2. Servicer Host: Sends Visa and MasterCard Card Transactions (and, if applicable, Discover Network Transactions) to Interchange and other Card Transactions to the appropriate Issuer (e.g., American Express Transactions to American Express). If the Transactions are not sent to Interchange, go to step 4.

3. Interchange: Sends Transaction data to the appropriate Issuer.

4. Issuer: Posts the Transaction to the Cardholder’s account. The Issuer either sends to Interchange the difference between the Transaction amount and the Interchange fee charged to the Servicer, or sends the funds to the Merchant’s DDA (see step 7).

5. Interchange: Sends the difference between the Transaction amount and the Interchange Fees to the Servicer Host.

6. Servicer Host: Sends a message to the Automated Clearing House (ACH) to pay the Merchant for the Transactions.

7. Automated Clearing House (ACH): Sends the funds from Servicer to the Merchant’s DDA via electronic transfer. Fees are debited from the Merchant’s DDA on a monthly or daily basis.

Follow these guidelines when you process Transactions:

To process a Transaction, follow these steps:

1. Follow all Prompts and Enter all Data Elements. You must include required elements to receive approval for Transactions and you can include optional data elements to qualify for better Interchange rates.

For example: Under the current data requirements, Visa Business, Visa Corporate, and Visa Purchasing Card Transactions must include sales tax information to qualify for the Level II Interchange Rate, where applicable. Purchasing Cards only qualify if the customer code is also included in the Transaction.

2. Make Sure the Card is Valid. Check the Card’s expiration date and other features to ensure that the Card is valid. Refer to Chapter 4, Identifying Valid Cards for validation information. Refer to Chapter 4, Preventing Card Fraud for additional loss-prevention information.

3. Swipe the Card Through the POS Device. If the Card is successfully swiped, the POS Device may prompt you to enter the last four digits of the Card number. This process compares the account number in the Magnetic Stripe with the account number embossed on the Card.

If the POS Device cannot read the Magnetic Stripe, press the appropriate key to initiate a manual Transaction. When you are prompted by the POS Device, enter the Card number and expiration date embossed on the front of the Card. Make an Imprint of the Card on a paper Transaction Receipt to prove that the Card was present during the Transaction. Keep the Imprinted Transaction Receipt with the electronically printed Transaction Receipt from the POS Device.

Ensure that the paper Transaction Receipt contains all of the information related to the Transaction, such as the Transaction amount, Transaction Date, Merchant information, Authorization Code, and Cardholder’s signature.

4. Enter the Amount of the Transaction. When prompted by the POS Device, enter the amount of the Transaction using the numeric key pad. You do not need to include a decimal point.

For Example: Enter $125.00 by pressing the 1-2-5-0-0 keys consecutively, and then pressing the ENTER key. The POS Device displays a message that indicates when the Transaction is being processed for Authorization.

5. Obtain the Authorization Code. If the Transaction is approved, the Approval Code prints on the Transaction Receipt. If a printer is not present, the POS Device displays the Approval Code.

If you have to Imprint the Card, remember to record the Approval Code on the Transaction Receipt.

If the Transaction is declined, the POS Device displays “Declined” or “Declined-Pick-Up”. In these cases, you should ask for another form of payment.

If the POS Device displays a “Referral” or “Call Auth” message, call the toll-free Voice Authorization telephone number (located on a sticker on your POS Device) and follow the operator’s instructions. If you receive an Approval Code, you must enter it into your POS Device to complete the Transaction. If Authorization is declined, the Voice Authorization Center may ask you to retain the Card. If this occurs, follow the operator’s instructions. A reward may be paid for the return of a Card at the Voice Authorization Center’s request.

6. Have the Cardholder Sign the Transaction Receipt, and then Compare Signatures. In Card Present Transactions, Transaction Receipts must be signed by the Cardholder unless otherwise specified under separate criteria for a Credit Card Association program (e.g., No Signature Required Programs). Compare the signature on the Transaction Receipt with the signature on the back of the Card. If you cannot tell whether the signatures are similar, ask to see another form of identification and compare the second signature with the others. You may also compare the appearance of the Cardholder with the picture on his or her identification cards. Merchant must not honor any Card if: (i) the Card has expired; (ii) the signature on the Transaction Receipt does not correspond with the signature on the Card or if the signature panel on the Card is blank, or uses language to the effect of “see id”; or (iii) the account number embossed on the Card does not match the account number on the Card’s magnetic stripe. If you are still suspicious of the Transaction or the Cardholder, you may perform a Code 10 Authorization. Refer to Chapter 4, Identifying Valid Cards for more information.

7. Return the Card and the Customer Copy of the Transaction Receipt to the Cardholder. When the Transaction is complete, return the Card to the Cardholder, along with the Customer copy of the Transaction Receipt. Keep the Merchant copy of the Transaction Receipt for your records.

Surcharges. Discover Network, Visa and MasterCard permit merchants in the U.S. to add a surcharge to a Credit Card Transaction amount, subject to their respective Credit Card Rules. As a result, if permitted, Merchant may add an amount to the posted price of goods or services Merchant offers as a condition of paying with a Discover Network, Visa and MasterCard Credit Card. If Merchant is permitted to and elects to apply a surcharge to its Discover Network, Visa and MasterCard Credit Card Transactions, Merchant must abide by all Payment Network Regulations applicable to surcharging, including, but not limited to, any advance notice requirements. In addition, Merchant may be required to register with Discover Network, Visa and/or MasterCard prior to surcharging any Credit Card Transactions. Registration requirements are set forth in the applicable Credit Card Rules and may be available through the applicable Payment Network websites.

This paragraph does not prohibit Merchant from offering a discount or in-kind incentive to induce a person to pay by cash, Credit Card, Debit Card or any other method of payment.

Return Policy. Merchant must properly disclose to the Cardholder, at the time of the Transaction and in accordance with the Card Rules, any limitation Merchant has on accepting returned merchandise.

No Claim Against Cardholder. Unless Servicer or Member refuses to accept a Transaction Receipt or revokes their prior acceptance of a Transaction Receipt (after receipt of a Chargeback or otherwise): (i) Merchant will not have any claim against, or right to receive payment from, a Cardholder in any Transaction; and (ii) Merchant will not accept any payments from a Cardholder relating to previous charges for merchandise or services included in a Transaction Receipt, and if Merchant receives such payments, Merchant will promptly remit them to Servicer.

A Transaction Receipt is a paper or electronic record of the purchase of goods or services from a Merchant by a Cardholder using a Card. You must provide the Cardholder with a Transaction Receipt for his or her personal records.

Transaction Receipts are required for all Transaction types and must be retained for a minimum of two (2) years (or such longer period as the Card Rules or the Laws may require). Transaction Receipts should be stored in a safe, secure area and organized in chronological order by Transaction Date.

An Electronic Transaction Receipt must contain the following information:

For Card Present Transactions, if the following information embossed or printed on the Card is not legibly imprinted on the Transaction Receipt, Merchant will legibly reproduce on the Transaction Receipt the: (i) Cardholder’s name; (ii) Card account number; (iii) Card expiration date; and (iv) Merchant’s name and place of business.

For Card Present Transactions, if Merchant authorizes and presents Transactions electronically and Merchant’s POS Device is unable to read the Magnetic Stripe on the Card, Merchant must generate a manual Transaction Receipt containing the information set forth below under “Manual Transaction Components,” in addition to key-entering the Transaction into the POS Device for processing.

A manual Transaction Receipt must contain the following information:

NOTE: If the Cardholder presents an unembossed Card and the POS Device cannot read the Magnetic Stripe then the Merchant must request another form of payment. Manual Transaction Receipts are prohibited on Transactions involving an unembossed Card.

The Merchant must provide a complete and legible copy of the Transaction Receipt to the Cardholder in the following manner:

Electronic Commerce Transaction Receipts must not include the Card’s account number.

If Merchant utilizes electronic Authorization and/or data capture services, Merchant will enter the data related to Transactions into a POS Device and settle the Transactions and transmit the data to Servicer or its designated agent in the form specified by Servicer no later than the close of business on the date the Transactions are completed. If Member or Servicer requests a copy of a Transaction Receipt, Credit Transaction Receipt, or other Transaction evidence, Merchant must provide it within the time frame specified in the request.

Merchant will include a description and total amount of goods and services purchased in a single Transaction on a single Transaction Receipt unless: (i) partial payment is entered on the Transaction Receipt and the balance of the Transaction amount is paid in cash or by check at the time of the Transaction; or (ii) a Transaction Receipt represents an advance deposit in a Transaction completed in accordance with the Agreement and the Card Rules.

Merchant must execute one Transaction Receipt when processing the deposit Transaction and a second Transaction Receipt upon processing the balance of the Transaction. Merchant will note the words “deposit” or “balance” on the applicable Transaction Receipt, as appropriate. Merchant will not deposit the Transaction Receipt labeled “balance” until the goods have been delivered to the Cardholder or until Merchant has fully performed the services.

Merchant represents and warrants to Member and Servicer that Merchant will not rely on any proceeds or credit resulting from future delivery Transactions to purchase or furnish goods or services. Merchant will maintain sufficient working capital to provide for the delivery of goods or services at the agreed upon future date, independent of any credit or proceeds resulting from Transaction Receipts or other Credit Transaction Receipts in connection with future delivery Transactions.

Card Not Present Transactions include Mail Order (MO), Telephone Order (TO), and Electronic Commerce (EC) Transactions. These Transactions occur when the Card is not physically presented to the Merchant at the time of a sale. You must be authorized by us to process Card Not Present Transactions.

If more than twenty percent (20%) of your Transactions are MO/TO, you must apply for a separate MID for those Transactions. If more than one percent (1%) of your Transactions are Electronic Commerce orders, you must also apply for a separate MID for those Transactions.

Merchant understands that Transactions processed via MO/TO are high risk and subject to a higher incidence of Chargebacks. Merchant is liable for all Chargebacks and losses related to MO/TO Transactions. Merchant may be required to use an address verification service (“AVS”) on MO/TO Transactions. AVS is not a guarantee of payment and the use of AVS will not waive any provision of the Agreement or validate a fraudulent Transaction. Merchant will obtain the expiration date of the Card for a MO/TO Transaction and submit the expiration date when requesting Authorization of the Transaction. For MO/TO Transactions, Merchant will type or print legibly on the signature line of the Transaction Receipt the following applicable words or letters: telephone order or “TO,” or mail order or “MO,” as appropriate. Servicer recommends that Merchant obtain a signed Transaction Receipt or other proof of delivery signed by Cardholder for MO/TO Transactions.

Merchant may process Electronic Commerce Transactions only if the Transactions have been encrypted by Servicer or a third party vendor acceptable to Servicer and Member. Merchant understands that Transactions processed via the Internet are high risk and subject to a higher incidence of Chargebacks. Merchant is liable for all Chargebacks and losses related to Electronic Commerce Transactions, whether or not such Transactions have been encrypted. Encryption is not a guarantee of payment and does not waive any provision of the Agreement or otherwise validate a fraudulent Transaction. Servicer recommends that Merchant obtain a signed Transaction Receipt or other proof of delivery signed by the Cardholder for all Electronic Commerce Transactions. All communication costs and compliance with Laws related to Electronic Commerce Transactions will be Merchant’s responsibility. Merchant understands that Servicer will not manage the telecommunications link for Electronic Commerce Transactions and that it is Merchant’s responsibility to manage that link. Merchant authorizes Servicer and Member to perform an annual audit and examination of Merchant’s website and such other due diligence review as required by the Payment Network Regulations for Electronic Commerce Merchants.

Requirements. Merchant’s website must contain all of the following information: (a) prominently display the name of the Merchant; (b) prominently identify the name of the Merchant as displayed on the website as both the Merchant and as the name that will appear on the Cardholder statement; (c) display Merchant name information as prominently as any other information depicted on the website, other than images of the products or services being offered for sale; (d) complete description of the goods or services offered; (e) returned merchandise and refund policy; (f) customer service contacts, including electronic mail address and/or telephone number; (g) complete address (street address, city, state, zip code, and country) of the permanent establishment of the Merchant’s business; (h) complete address of the permanent establishment of the Merchant’s business on either the checkout screen (which displays the total purchase amount) or within the sequence of website pages presented to the Cardholder during the checkout process; (i) Transaction currency (such as U.S. or Canadian dollars); (j) export or legal restrictions, if known; (k) delivery policy; (l) Customer data privacy policy; and (m) Merchant’s method of Transaction security such as Secure Sockets layer (SSL) or 3-D Secure. If Merchant stores Card account numbers, expiration dates, or other personal Cardholder data in a database, Merchant must follow the applicable Payment Network Regulations on securing such data. Merchant may not retain or store CVV2/CVC2/CID data after authorization for record keeping or additional authorization processing. A Merchant must not refuse to complete an Electronic Commerce Transaction solely because the Cardholder does not have a digital certificate or other secured protocol.

Shipped Goods. For goods to be shipped on Electronic Commerce Transactions, Merchant may obtain authorization up to seven (7) days prior to the shipment date. Merchant need not obtain a second authorization if the Transaction Receipt amount is within fifteen percent (15%) of the authorized amount, provided the additional amount represents shipping costs.

Card Not Present Transactions pose a higher risk of fraud and Chargebacks, so it is important that you take precaution in processing these Transactions. Follow these guidelines prior to processing a Card Not Present Transaction, as applicable:

NOTE: You must not retain or record the CVV2/CVC2/CID data element beyond the original Authorization request. Further, the CVV2/CVC2/CID data element must not be printed on the Transaction Receipt or on any document given to the Cardholder.

In addition to the Transaction Receipt requirements set out in Chapter 2, Processing Transactions, a Card Not Present Transaction Receipt must also contain:

Do not settle a Transaction before shipping the goods. This increases the risk of a Chargeback to the Merchant and is prohibited by the Agreement.

Do not retain magnetic stripe data except for first time use.

Follow these steps for manual Transaction Receipts:

1. Write the Cardholder’s Name and Card Number on the Transaction Receipt. Refer to Chapter 2, Processing Transactions – Electronic Transaction Components for information on Transaction Receipt requirements. In addition to the electronic Transaction components requirements, a manual Transaction Receipt for a Card Not Present Transaction may include the full Card account number and expiration date and must include the Cardholder’s billing address (and shipping address, if different) and telephone number. Do not record CVV2/CVC2/CID data elements on the Transaction Receipt.

2. Record the Order Type on the Transaction Receipt. Write one of the following on the signature line of the Transaction Receipt:

If you are using a POS Device to generate a Transaction Receipt for a Card Not Present Transaction, enter the Transaction into the device by following these steps:

1. Press the appropriate key on your POS Device to initiate the Transaction.

2. When prompted, enter the Card number.

3. When prompted again, enter the Card expiration date.

4. Finally, when prompted, enter the Transaction amount.

5. Record the Authorization Code on the Transaction Receipt. Refer to Chapter 2, Processing Transactions – Transaction Receipts for more information.

The use of CVV2/CVC2/CID and AVS can lessen your risk of Chargebacks by providing you with additional information to assist with your decision on whether or not to process a Card Not Present Transaction.

NOTE: The use of CVV2/CVC2/CID and AVS will not relieve you of liability for Chargebacks. Remember, you bear the risk of loss associated with any Chargeback.

If you are using these services, follow the next two steps prior to processing a Transaction.

1. Verify the Card Identification Number (CVV2/CVC2/CID) Printed on the Front or Back of the Card (at the end of the Card Account Number in the Signature Panel), as Applicable to the Specific Card Type. If your POS Device is set up for CVV2/CVC2/CID and if the CVV2/CVC2/CID number is provided at the time of Authorization, the Issuer returns either a “match” or a “no match” response. “Match” means it is more likely that the Card is present and in the hands of the Cardholder at the time of the Transaction. “No match” means you should consider whether or not to process the Transaction. Even though you receive an Approval Code with a “no match” response, the Approval Code is not a guarantee of payment. The decision to process a Transaction, regardless of the response received, is up to you, because you are responsible for any risk associated with processing a Transaction.

NOTE: You must not retain or record the CVV2/CVC2/CID data element beyond the original Authorization request. Further, the CVV2/CVC2/CID data element must not be printed on the Transaction Receipt or on any document given to the Cardholder.

Most Customers do not know where the CVV2/CVC2/CID code is located on the Card. To assist a Customer, have him or her locate the last three (or four) alphanumeric characters in the signature panel on the back of his or her Card for Discover Network, Visa or MasterCard Card types or on the front of his or her Card for American Express Card types.

Refer to Chapter 4, Unique Card Characteristics, for more details concerning the Card Identification Number. The following table sets forth CVV2/CVC2 response codes.

| Code | Definition |

| Space | CVV2 processing not requested |

| M | CVV2/CVC2 Match |

| N | CVV2/CVC2 not matched |

| P | Not processed |

| S | CVV2 should be printed on the card, but it was indicated that the value was not present |

| U | Issuer does not support CVV2 |

| X | Service provider did not respond |

2. Verify the Cardholder’s Address by Using the Address Verification Service (AVS). If your POS Device is set up for AVS, it prompts you to enter the numeric portion of the Cardholder’s billing address and the five digit zip code to verify that the individual providing the Card account number is the Cardholder. The AVS result code indicates whether the address given by the Cardholder matches (exactly, partially, or not at all) the address that the Issuer has on file for the Card. “Exactly” means it is more likely that the Card is being used by the authorized Cardholder. “Partially” or “not at all” means you should consider whether or not to process the Transaction. The decision to process a Transaction, regardless of the response received, is up to you, as you are responsible for any risk associated with processing a Transaction. Even though you will receive an Approval Code following a “no match” response, the Approval Code is not a guarantee of payment. The following table sets forth AVS response codes.

| Code | Definition |

| A | Address (street) matches – ZIP Code does not |

| B | Street address match, postal code in wrong format (international issuer) |

| C | Street address and postal code in wrong formats |

| D | Street address and postal code match (international issuer) |

| E | Error response for Merchant Category Code (SIC) |

| G | Card issued by a non-U.S. issuer that does not participate in the AVS system |

| I | Address information not verified by international issuer |

| M | Street address and postal code match (international issuer) |

| N | No match on address (street) or ZIP Code |

| O | No response sent |

| P | Postal codes match, Street address not verified due to incompatible formats |

| R | Retry, system is unavailable or timed out |

| S | Service not supported by issuer |

| U | Address information is unavailable (domestic issuer) |

| W | Nine-digit ZIP Code matches – Address (street) does not match |

| X | Exact AVS Match |

| Y | Address (Street) and five digit Zip match |

| Z | Five-digit zip matches – address (street) does not match |

NOTE: For more information about CVV2/CVC2/CID and AVS, contact Merchant Services.

For more information about processing Card Not Present Transactions, call the following numbers:

The information provided by calling these numbers may allow you to verify a Cardholder’s address and obtain the Issuer’s telephone number.

We supply you with the materials and forms that you need to process Discover Network, Visa or MasterCard Transactions using paper drafts. You must maintain a supply of these materials. Refer to Chapter 24, Supplies for more information.

Before you process a paper draft, please follow the guidelines under Transaction Processing Proceduresearlier in this Chapter.

To correctly process a paper Transaction Receipt, follow these steps:

1. Make Sure the Card is Valid. Check the Card’s expiration date and other features to ensure that the card is valid. Refer to Chapter 4, Identifying Valid Cards for validation information. Refer to Chapter 4, Preventing Card Fraud for additional loss-prevention information.

2. Imprint the Transaction Receipt. Make a legible Imprint of the Card on all copies of the Transaction Receipt.

3. Call for Authorization. Call the Voice Authorization number provided on the sticker on your POS Device and have the following information available:

4. Write the Approval Code in the Space Provided on the Transaction Receipt. The Approval Code is required.

5. Have the Cardholder Sign the Transaction Receipt, and then Compare Signatures. Compare the signature on the Transaction Receipt with the signature on the back of the Card. If you cannot tell whether the signatures are similar, ask to see another form of identification and compare the second signature with the others. You may also compare the appearance of the Cardholder with the picture on his or her identification cards. If you are still suspicious of the Transaction or the Cardholder, you may perform a Code 10 Authorization. Refer to Chapter 4, Identifying Valid Cards for more information.

6. Return the Card and the Cardholder Copy of the Transaction Receipt to the Cardholder. When the Transaction is complete, return the Card to the Cardholder, along with the Cardholder copy of the Transaction Receipt. Make sure to keep the Merchant copy of the Transaction Receipt for your records.

7. Storage of Paper Drafts. It is important to keep copies of your Transaction Receipts in a safe place, filed by Transaction Date. This is especially important for quickly locating a receipt if questions arise. The PCI Data Security Standard sets out the requirements on how to handle the storage of paper drafts that contain Cardholder information.

Visit http://www.pcisecuritystandards.org/security_standards/pci_dss.shtml or contact Customer Service at 1-800-725-1243 for more information.

Credit Transaction Receipt. Merchant must issue a Credit Transaction Receipt, instead of issuing cash or a check, as a refund for any previous Transaction. Member or Servicer will debit the DDA for the total face amount of each Credit Transaction Receipt submitted to Servicer. Merchant must not submit a Credit Transaction Receipt relating to any Transaction Receipt not originally submitted to Servicer, and Merchant must not submit a Credit Transaction Receipt that exceeds the amount of the original Transaction Receipt. Merchant must, within the time period specified by applicable Laws or the Card Rules, whichever time period is shorter, provide Servicer with a Credit Transaction Receipt for every return of goods or forgiveness of debt for services that was the subject of a previous Transaction in accordance with the Card Rules.

Revocation of Credit. Member or Servicer may, in their reasonable discretion, refuse to accept any Credit Transaction Receipt for processing.

Reprocessing. Merchant must not resubmit or reprocess any Transaction that has been charged back.

Refunds for a Transaction must be processed by issuing a credit to the Card on which the original purchase was made. You must also prepare a Credit Transaction Receipt for the amount of credit issued. Do not refund a Card purchase with cash or check. Do not refund cash or check purchases to a Card.

If you have a special policy regarding returns or refunds, make sure that the policy is:

If you are processing an even exchange, no action is necessary. However, if an exchange involves merchandise of greater or lesser value, you must issue a Transaction Receipt or a Credit Transaction Receipt for the difference. If you prefer, you may instead give a full refund to the Cardholder for the original Transaction amount and process the exchange as a new Transaction.

With respect to Debit Card, PIN-authorized Debit Card, and Prepaid Card Transactions, Merchants operating in the Merchant Category Codes in the table below must:

1. For all Card Present Transactions occurring at an attended POS Device or at a Cardholder-activated POS Device identified with MCC 5542 (Automated Fuel Dispensers), support partial approvals;

2. For all Transactions, support full and partial reversals; and

3. For all Card Present Transactions occurring at an attended POS Device and conducted with a Prepaid Card, support account balance responses;

each as further described below.

| MCC |

| 4111 Transportation—Suburban and Local Commuter Passenger, including Ferries |

| 4812 Telecommunication Equipment including Telephone Sales |

| 4814 Telecommunication Services |

| 4816 Computer Network/Information Services |

| 4899 Cable, Satellite, and Other Pay Television and Radio Services |

| 5111 Stationery, Office Supplies |

| 5200 Home Supply Warehouse Stores |

| 5300 Wholesale Clubs |

| 5310 Discount Stores |

| 5311 Department Stores |

| 5331 Variety Stores |

| 5399 Miscellaneous General Merchandise Stores |

| 5411 Grocery Stores, Supermarkets |

| 5499 Miscellaneous Food Stores — Convenience Stores, Markets, Specialty Stores and Vending Machines |

| 5541 Service Stations (with or without Ancillary Services) |

| 5542 Fuel Dispenser, Automated |

| 5732 Electronic Sales |

| 5734 Computer Software Stores |

| 5735 Record Shops |

| 5812 Eating Places, Restaurants |

| 5814 Fast Food Restaurants |

| 5912 Drug Stores, Pharmacies |

| 5921 Package Stores, Beer, Wine, and Liquor |

| 5941 Sporting Goods Stores |

| 5942 Book Stores |

| 5943 Office, School Supply and Stationery Stores |

| 5964 Direct Marketing—Catalog Merchants |

| 5965 Direct Marketing—Combination Catalog—Retail Merchants |

| 5966 Direct Marketing—Outbound Telemarketing Merchants |

| 5967 Direct Marketing—Inbound Telemarketing Merchants |

| 5969 Direct Marketing—Other Direct Marketers—not elsewhere classified |

| 5999 Miscellaneous and Specialty Retail Stores |

| 7829 Motion Picture-Video Tape Production-Distribution |

| 7832 Motion Picture Theaters |

| 7841 Video Entertainment Rental Stores |

| 7996 Amusement Parks, Carnivals, Circuses, Fortune Tellers |

| 7997 Clubs—Country Membership |

| 7999 Recreation services—not elsewhere classified |

| 8011 Doctors — not elsewhere classified |

| 8021 Dentists, Orthodontists |

| 8041 Chiropractors |

| 8042 Optometrists, Ophthalmologists |

| 8043 Opticians, Optical Goods, and Eyeglasses |

| 8062 Hospitals |

| 8099 Health Practitioners, Medical Services — not elsewhere classified |

| 8999 Professional Services—not elsewhere classified |

| 9399 Government Services —not elsewhere classified |

Partial Approvals. When a Debit Card, PIN-authorized Debit Card, or Prepaid Card Authorization request is sent, the issuer can respond with an approval amount less than the requested amount. When the approved amount is less than the originally requested amount, Merchant should prompt the Customer to pay the difference with another form of payment. If the Customer does not wish to proceed with all or part of the Transaction (or if the Transaction “times out”), the Merchant must initiate an authorization reversal Transaction.

Full and Partial Authorization Reversals. An “authorization reversal” is a real-time Transaction initiated when the Customer decides that it does not want to proceed with the Transaction or if the Merchant cannot complete the Transaction for any reason (e.g., the item is out of stock, the Transaction “times out” while waiting for the Authorization response, etc.). To initiate an authorization reversal, the Transaction must have already been authorized but not submitted for Settlement. If the Transaction has already been submitted for clearing, then the Merchant should initiate a void, refund, or other similar Transaction so that the Customer’s open-to-buy is freed up and the available balance is restored. A partial authorization reversal should be initiated whenever the Merchant determines that the final Transaction amount will be less than the amount of the Authorization.

Authorization reversals must be processed by the Merchant within 24 hours of the original Authorization request for Card Present Transactions and within 72 hours of the original Authorization Request for Card Not Present Transactions; provided, however, that Merchants in hotel, lodging, cruise line and vehicle rentals are exempt from this requirement.

Account Balance Response. For some Prepaid Cards, the Issuer is required to include the remaining available balance on the Cardholder’s account in the Authorization response message. If the remaining available balance is included, the Merchant must print it on the Transaction Receipt or display it on a Customer facing POS Device.

Debit Card Rules. Merchant shall comply with and be bound by the Debit Card Rules, which are incorporated by this reference as if fully set forth herein. Except as otherwise provided below, Merchant must comply with the general Card acceptance and Transaction processing provisions in this Chapter when accepting Debit Cards. The Debit Card Rules are confidential information of the Payment Networks, and Merchant shall not disclose the Debit Card Rules to any Person except as may be permitted under the Agreement or under requirements of Laws.

Use and Availability of POS Devices and PIN Pads.

No Minimum or Maximum. Merchant shall not establish minimum or maximum Debit Card Transaction amounts except to establish a maximum cash back dollar amount not to exceed $200.00 or such lower amount as may be required under applicable Payment Network Rules.

Pre-Authorization Requests. Merchant may initiate pre-authorization requests pursuant to the following procedures:

Debit Card Transactions. Merchants that accept PIN-authorized Debit Cards shall support the following Debit Card Transactions:

Merchant may also support the following Debit Card Transactions if supported by the applicable EFT Network:

Prohibited Transactions. Merchant shall initiate Transactions only for products or services approved by Servicer. In no event shall Merchant initiate, allow, or facilitate a gambling or gaming transaction, or fund a stored value account for such purposes.

Transaction Receipt Requirements. At the time of any Debit Card Transaction (other than a balance inquiry or pre-authorization request), Merchant shall make available to each Cardholder a Transaction Receipt that complies fully with all Laws and containing, at a minimum, the following information:

Merchandise Returns. Merchant may electronically perform a merchandise return (if permitted by the applicable EFT Network) for a Debit Card Transaction only at the same Merchant named on the Transaction Receipt where the original Debit Card Transaction was initiated. If permitted, a merchandise return requires the following procedures:

For all merchandise returns or any other debit return initiated through Merchant’s POS Device or account, Merchant bears all responsibility for such Transaction even if fraudulent.

Balance Inquiries. Merchant may accommodate balance inquiries if the applicable EFT Network and the Issuer support the balance inquiry function, provided that the Merchant requires that the Cardholder enter their PIN on the PIN Pad and insert and “swipe” the Debit Card through the POS Device.

Purchase with Cash Back. Merchant may offer purchase with cash back Transactions pursuant to the following procedures:

Technical Problems. Merchant shall ask a Cardholder to use an alternative means of payment if the Servicer Debit System, the POS Device, or the PIN Pad is inoperative, the electronic interface with any EFT Network is inoperative, or the magnetic stripe on a Debit Card is unreadable, and Merchant elects not to or is unable to store Debit Card Transactions.

Adjustment. A Debit Card Transaction may be adjusted if an error is discovered during Merchant’s end- of-day balancing only by means of a written request from Merchant to Servicer. The request for adjustment must reference a settled Debit Card Transaction that is partially or completely erroneous or a denied pre- authorize Transaction for which the pre-authorization request was approved. An adjustment must be completed within forty-five (45) days after the date of the original Debit Card Transaction.

Termination/Suspension. When requested by any EFT Network, in its sole discretion, Merchant will immediately take action to: (i) eliminate any fraudulent or improper Transactions; (ii) suspend the processing of Debit Card Transactions; or (iii) entirely discontinue acceptance of Debit Card Transactions.

Acceptance of Internet PIN-Based Card Transactions. This section describes certain special requirements applicable to Internet PIN-Based Card Transactions. Except as specifically provided in this section, Merchant shall comply with the general provisions of this Chapter regarding PIN-authorized Debit Card Transactions with respect to Internet PIN-Based Card Transactions. For the avoidance of doubt, Internet PIN-Based Card Transactions are Card Not Present Transactions. Therefore, notwithstanding anything in this Merchant Operating Guide to the contrary, Merchant is not required to “swipe” a Card in conjunction with any Internet PIN-Based Card Transaction and the Cardholder and the Card are not required to be present at the time of the sale.

International Network Requirements. If Merchant supports Internet PIN-Based Card Transactions, Merchant shall comply with and be bound by the International Network Requirements and Internet PIN- Based Card Transaction Documentation, which are incorporated by this reference as if fully set forth herein. The International Network Requirements and Internet PIN-Based Card Transaction Documentation are confidential information of the International Networks or of Servicer, as applicable, and Merchant shall not disclose the International Network Requirements or the Internet PIN-Based Card Transaction Documentation to any Person except as may be permitted under the Agreement or under requirements of Laws.

Use and Availability of Internet PIN Pads.

Transaction Receipt Requirements. Merchant shall ensure that any receipt provided for an Internet PIN-Based Card Transaction includes:

Refunds / Cashback / Balance Inquiries. If permitted by the applicable International Network or EFT Network, Merchant may electronically perform a merchandise return or refund for an Internet PIN-Based Card Transaction. However, credits, balance inquiries and purchases with cash back cannot be performed as Internet PIN-Based Card Transactions.

Technical Problems. Merchant shall ask a Cardholder to use an alternative means of payment if the Servicer Debit System, the Internet PIN Pad, or the electronic interface with any EFT Network or International Network is inoperative.

Merchant may solicit the following other Transaction types provided that (a) Merchant discloses such method of processing to Servicer in the Merchant Application or otherwise in writing, (b) Merchant has been approved by Servicer to submit such Transactions, and (c) Merchant meets the additional requirements for the applicable type of Transaction set out below. If Merchant completes any of these Transaction types without having received Servicer’s approval, then Merchant will be in breach of the Agreement and Servicer may terminate the Agreement in addition to any other remedies available under the Agreement, Laws, or Payment Network Regulations, and Merchant may pay a surcharge on each such Transaction.

Recurring Payments are Transactions for which a Cardholder provides written permission or electronic authorization to a Merchant to periodically charge his or her Card for recurring goods or services (e.g., monthly membership fees, utility bills, insurance premiums, or subscriptions). When processing Recurring Payments, you must obtain a separate Authorization Code for each Transaction.

Pre-authorized Orders are Transactions in which the Cardholder provides written or electronic authorization to charge his or her Card, one or more times, at a future date. You must be authorized by us to process Pre-authorized Orders.

You must obtain a signed order form or other written agreement from the Cardholder for all Recurring Payments and Pre-authorized Orders. The order form or agreement must contain the following information:

You must keep a copy of the order form or written agreement for the duration of the recurring service. You must also provide a copy of the order form or agreement for Recurring Payments or Pre-authorized Orders to us upon request. A new order form or written agreement with the Cardholder is needed when a Recurring Payment is renewed.

Recurring Transaction Requirements. Merchant will not complete any recurring Transaction after receiving: (i) a cancellation notice from the Cardholder; (ii) a notice from Servicer or Member that authority to accept recurring Transactions has been revoked; or (iii) a response that the Payment Device is not to be honored. Merchant is responsible for ensuring its compliance with Laws with respect to recurring Transactions.

Limitations on the Resubmission of Recurring Transactions. In some limited instances, Merchant may resubmit a declined preauthorized recurring Transaction up to four (4) times within sixteen (16) calendar days of the original Authorization request, provided that the decline response is one of the following: (i) authorization denied; (ii) insufficient funds; (iii) exceeds approval amount limit; or (iv) exceeds withdrawal frequency.

Recurring Transaction Receipts. Merchant must print legibly on the Transaction Receipt the words “Recurring Transaction.” Merchant must obtain the Cardholder’s signature, which may be an electronic signature or other similar authentication that is effective under applicable Laws, on the Transaction Receipt. Merchant must also include the frequency and duration of the Recurring Transaction authorization, as agreed to by the Cardholder, on the Transaction Receipt.

Electronic Commerce Recurring Transactions. In addition to the above, for an Electronic Commerce Transaction, Merchant must also provide a simple and easily accessible online cancellation procedure that complies with Laws, if the Cardholder’s request for goods or services was initially accepted online.

Recurring Transactions with Varying Amounts. For Recurring Transactions of varying amounts, all of the following apply: (i) the order form must allow the Cardholder to specify a minimum and maximum Transaction amount to be charged, unless the Cardholder will be notified of the amount and date of each charge, as specified in the remainder of this section; (ii) Merchant must inform the Cardholder of their right to receive, at least ten (10) calendar days prior to each scheduled Transaction Date, written notification of the amount and date of the next charge; and (iii) the Cardholder may choose to receive the notification in any of the following ways: (a) for every charge; (b) when the Transaction amount does not fall within the range of amounts specified on the order form; or (c) when the Transaction amount will differ from the most recent charge by more than an agreed upon amount. Merchant is responsible for ensuring that all communications with, and disclosures to, Cardholders comply with Laws.

To perform a Pre-authorized Order, follow these specific guidelines:

While you may process the Transaction for the “Deposit” before delivery of the goods and/or services, you may not process the “Balance” of the Transaction until the goods and/or services are delivered.

Quasi-Cash Transactions represent the sale of items that are directly convertible to cash. Examples of Quasi-Cash Transactions include:

You must be authorized by us to process Quasi-Cash Transactions. No Merchant may process a Quasi- Cash Transaction as a cash disbursement.

In addition to the general requirements described in Chapter 2, Transaction Receipts, Merchants processing Quasi-Cash Transactions must:

The Contactless Transaction requirements are as follows:

Participation. Merchant is responsible for:

1. Ensuring that all POS Devices that accept Contactless Cards for Transactions meet the applicable Credit Card Association specifications, are approved by Servicer and/or the applicable Credit Card Associations for use with Contactless Cards, and are configured to transmit the data elements required for Contactless Transactions.

2. Complying with all Payment Network Regulations applicable to Transactions conducted with Contactless Cards, including all operating requirements, technical guides and other requirements specified by the applicable Credit Card Associations in connection with the acceptance of Contactless Cards.

Registration. It is Merchant’s responsibility to ensure that it is eligible and has been approved by Servicer to accept Contactless Cards, and that Merchant has been registered with the applicable Credit Card Associations to participate in their respective Contactless Card payment program(s).

Processing. Merchant is responsible for:

1. Providing any data in the Authorization request as required by the applicable Credit Card Associations.

2. Transmitting the full and unaltered contents of Track 1 or Track 2 data of the Card’s Magnetic Stripe or Contactless payment chip in the Authorization request.

3. Ensuring that Transactions are not processed as Contactless Transactions if currency conversion is performed.

4. Submitting only a single Authorization per clearing Transaction.

Merchants that are eligible for both a Credit Card Association’s No Signature Requirement Program and to accept Contactless Cards may combine these programs to further enhance the benefits of accepting Contactless Cards and participating in a No Signature Required Program.

Chapter 3

This Chapter describes how to settle your daily Transactions. The guidelines for Settlement within this Chapter can help you:

To settle the daily Batch, perform the following steps:

1. Total the day’s Transaction Receipts and Credit Transaction Receipts.

2. Verify that the Transaction Receipts equal the POS Device totals. You may print a report from your POS Device to assist you with balancing. For more information about balancing, refer to the instructions that came with your POS Device.

If the totals do not balance, then do the following:

3. Close the Batch according to the instructions for your POS Device.

NOTE: Submit your Transactions for processing daily to obtain the most favorable pricing.

If you are not using a POS Device, you must deposit Discover Network, Visa and MasterCard Transaction Receipts or Credit Transaction Receipts within three (3) business days, except:

1. The Transaction Receipts or Credit Transaction Receipts must not be presented until after the products are shipped or the services are performed unless, at the time of the Transaction, the Cardholder agrees to a properly disclosed delayed delivery of the products or services.

2. When the Merchant receives Cardholder authorization for a delayed presentment (in which case the words “Delayed Delivery” must be noted on the Transaction Receipt or Credit Transaction Receipt).

3. When the Merchant is obligated by law to retain the Transaction Receipt or Credit Transaction Receipt or return it to a Customer upon timely cancellation, in which case the Merchant should present the record within ten (10) business days after the Transaction date.

4. When the Merchant has multiple locations and uses a central facility to accumulate and present records to Servicer, in which event the Merchant must present the record in accordance with applicable law and, in any event, within thirty (30) calendar days of the Transaction date.

Please include a Batch Header with your Transaction Receipts.

To prepare a paper deposit, follow these steps:

1. Place your Merchant Identification Card and the Batch Header in the Imprinter.

2. Imprint the information onto the Batch Header.

3. Enter the total number and dollar amount of Transaction Receipts. It is not necessary to separate the Discover Network, Visa and MasterCard Transaction Receipts.

4. Enter the total number and dollar amount of Credit Transaction Receipts.

5. Review the Transaction Receipts and Credit Transaction Receipts to make sure they bear legible Discover Network, Visa or MasterCard numbers and amounts. Visa uses 16-digit account numbers beginning with a “4” and MasterCard uses 16-digit account numbers beginning with a “5.” Discover Network uses 16-digit account numbers beginning with a “6.”

6. Enter the net amount of the Transaction Receipts and the Credit Transaction Receipts.

7. Fill in the date and your DDA (Demand Deposit Account) number.

8. Place the bank copy of all Transaction Receipts and Credit Transaction Receipts behind the Batch Header and insert them into the Merchant deposit envelope, which is addressed to the paper processing center. If you need additional Merchant deposit envelopes, please contact Merchant Services.

9. Retain a copy of the Batch Header, along with your copies of the Transaction Receipts and Credit Transaction Receipts for your records.

10. Make sure the paper processing center address is on the front of the envelope.

11. Mail the Merchant deposit envelope.

12. Store paper drafts appropriately. For storage requirements for paper drafts in compliance with the PCI Data Security Standard, visit: http://www.pcisecuritystandards.org/security_standards/pci_dss.shtml.

If we detect an imbalance between your Batch Header and the attached Transaction Receipts, we make an adjustment to your DDA and send you an adjustment notice. Remember, adjustments differ from Chargebacks. If you have any questions concerning an adjustment, contact Merchant Services.

The most common reasons for adjustments include:

Remember to reconcile your monthly Merchant Statements with your DDA statement, along with any adjustment notices you may have received.

Chapter 4

It is important to take steps to educate yourself and your staff to reduce your risk of accepting a counterfeit or fraudulent Card Transaction. Remember that you are responsible for all Chargebacks, including those for fraudulent Transactions. Fraudulent Card sales involve an invalid Card account number or, more commonly, a valid Card number presented by an unauthorized user. Fraud normally occurs within hours of the loss, theft, or compromise of a Card number or Card, and before most victims report the Card missing or discover the compromise.

If a Transaction is declined, do not request a Code 10 Authorization and do not complete the Transaction. However, if you receive an Approval Code but suspect a Card has been altered or is counterfeit, call the Voice Authorization Center and request a Code 10 Authorization (see Chapter 5, Code 10 Procedures).

The following sections provide tips to assist you in protecting yourself against fraud losses.

Common sense is the best guide for spotting suspicious behavior. Be sure you combine watchfulness with proper Card identification and validation techniques.

Be aware of customers who:

The increased use of Electronic Commerce, mail, and telephone orders has resulted in an increasing amount of fraud. If you accept Card Not Present Transactions, take caution if a customer attempts to:

You should be particularly careful if you sell products that are easily resold. For example, computers and computer equipment, printer cartridges, and jewelry are more susceptible to fraud than perishable items such as food—although criminals can victimize virtually any type of business.

NOTE: If you receive an order for a large purchase for delivery to a foreign country or to a freight forwarder, we recommend that you contact your Voice Authorization Center to request a Code 10 specifically identifying the Transaction as a large foreign shipment Transaction.

Cards share similar qualities to help identify their validity, and there are anti-fraud safeguards unique to each Card brand.

You should not accept a Card that is not signed. Many Card users write “Use other ID” (or something similar) in the signature panel because they believe it provides a higher level of security. This is not actually true, it simply allows a thief to sign his or her own name or use a fake ID with any signature.

If an unsigned Card is presented to you:

1. Inform the customer that the Card must be signed.

2. Have the customer sign the Card in your presence and provide a current, valid government ID that has been signed (such as a passport or driver’s license). Do not accept a temporary form of ID, such as a temporary driver’s license that does not have a photo.

3. Compare the signature on the ID to that on the Card.

4. If the customer refuses to sign the Card, do not complete the Transaction. Remember, you are liable for any Transaction processed with a fraudulent Card.

After you swipe a Card, the POS Device prompts you for specific information. The POS Device may also prompt you to enter the last four digits of the account number to verify that the embossed account number matches the number on the Magnetic Stripe (on the back of the Card). If the numbers do not match, the POS Device indicates a mismatch of the digits or an invalid Card. Do not accept the Card. Once you receive an Approval Code, verify that the Card number on the Transaction Receipt matches the number embossed on the Card. If it does not match, do not accept the Card.

These characteristics typically apply to most Card brands.

For the unique Card design elements specific to the Cards, please visit the following Card websites.

The following section identifies common Card tampering techniques. Although an American Express Card is used in the examples, these tampering methods are widespread among all Card types.

Characteristics of fraudulent Embossing include:

Figure 4-5. Example of Fraudulent Embossing

Characteristics of altered Magnetic Stripes include:

Be aware – not all Card fraud is committed by Customers. Sometimes employees engage in fraud using the following activities:

NOTE: Most POS Device products allow a Merchant to require a password in order to process a Credit Transaction.

To help prevent employee-related fraud, do the following:

Factoring (also known as Laundering) occurs when you process another person’s transactions through your Merchant account. Processing transactions which belong to another person or business is in violation of the Agreement and is prohibited by law in many states. Factoring may result in the termination of your Card acceptance privileges.

Be wary of the “fellow business person” who offers to pay you to process card transactions in return for a fee. These transactions are often questionable or fraudulent. These schemes typically result in a flood of Chargebacks which are debited from your DDA. By the time you realize this has occurred, the other business will most likely have relocated under a different name.

To protect you from these schemes and the devastating losses that ensue, educate yourself and your staff about this serious problem and immediately report Factoring propositions to us or to the U.S. Secret Service. Remember, you are responsible for all transactions processed using your MID, so make sure that all transactions processed through your account represent transactions between you and the Cardholder.

Merchant will not present for processing or credit, directly or indirectly, any Transaction not originated as a result of a transaction directly between Merchant and a Cardholder or any Transaction Merchant knows or should know to be fraudulent or not authorized by the Cardholder. Perpetrators of fraudulent Transactions will be referred to law enforcement officials. Merchant will not deposit any Transaction Receipt representing the refinancing of an existing obligation of a Cardholder.

Chapter 5

Code 10 is a term used by the Credit Card Associations to refer to suspicious or questionable Transactions, Cards, or Cardholders.

If you are suspicious of a Card Transaction, contact your Voice Authorization Center and request a Code 10 Authorization. Using the term “Code 10” allows you to call the Voice Authorization Center to question the Transaction without alerting the Cardholder. Follow the instructions given to you on how to proceed to minimize any discomfort between you and the Cardholder.

NOTE: Be alert to individuals who contact your business via phone or the Internet attempting to make large purchases for overseas shipment, direct or through a freight forwarder. These individuals may utilize one or more Cards in their “urgent” request. If you receive such a request, we encourage you to contact your Voice Authorization Center to request a Code 10, specifically identifying the Transaction as a large foreign shipment Transaction.

NOTE: Fraudulent transactions, even when authorized, are subject to Chargebacks, and final payment is not guaranteed.

To request a Code 10 Authorization for a Discover Network, Visa or MasterCard Transaction, call the telephone number on your Voice Authorization sticker (located on the POS Device). To request a Code 10 Authorization for American Express, call one of the following numbers:

If you are informed that a Card has been reported lost or stolen, or is otherwise invalid, do not complete the Transaction.

Card Recovery. If Merchant chooses to recover any Card, Merchant will use reasonable, peaceful means to recover any Card: (i) on Visa Cards, if the printed four digits below the embossed account number do not match the first four digits of the embossed account number; (ii) if Merchant is advised by Member (or its designee), the Issuer, or the designated voice authorization center to retain it; (iii) if Merchant has reasonable grounds to believe the Card is lost, stolen, counterfeit, fraudulent, or otherwise invalid, or its use is not authorized by the Cardholder; or (iv) for MasterCard Cards, if the printed four digits below the embossed account number do not match the first four digits of the embossed account number, or the Card does not have the “Twin Globes” hologram on the lower right corner of the Card face.

If you are instructed to retain the Card, follow these procedures:

Exception Processing

ATTN:Card Pick Up

Allegiance Merchant Services, Inc.

1401 Central Avenue

Charlotte, NC 28205

NOTE: Do not challenge the Card user. Avoid any physical confrontation with anyone who may be using a lost, stolen, or otherwise invalid Card. Do not jeopardize your safety or that of your employees or Customers.

Once the person leaves your location, note in writing his or her physical characteristics and any other relevant identification information. Keep in mind that a reward may be offered by the Issuer for the recovery and return of a lost, stolen, or otherwise invalid Card.

Chapter 6

A Cardholder or Issuer may dispute a Transaction for any number of reasons, including a billing error, a quality dispute, or non-receipt of goods and/or services. This Chapter describes the process for handling disputed Transactions by explaining Retrieval Requests and Chargebacks.

Disputes With Cardholders. All disputes by any Cardholder relating to any Transaction will be settled between Merchant and the Cardholder. Neither Servicer nor Member bears any responsibility for such Transactions or disputes, other than with respect to processing Chargebacks under the Payment Network Regulations.

Merchant is fully responsible for all Retrieval Requests and Chargebacks under the Payment Network Regulations. Upon receipt of a Retrieval Request or Chargeback from a Payment Network, Servicer and Member will forward such request or documentation to Merchant. Merchant is responsible for responding, as appropriate, to each Retrieval Request or Chargeback, including providing a copy of the relevant Transaction Receipt to Servicer. In addition, Merchant will cooperate with Servicer and Member in complying with the Credit Card Rules and Debit Card Rules regarding Retrieval Requests and Chargebacks. The following is a non-exhaustive list of reasons for which Merchant may incur a Chargeback. It is not a complete list of Chargeback reasons and is intended only to provide the most commonly encountered situations where a Chargeback may occur:

A Retrieval Request is made by the Issuer on behalf of the Cardholder for a copy of the Transaction Receipt. A Retrieval Request (also known as a Copy Request) most often occurs when a Cardholder:

The Retrieval Request notice you receive will include the following information to help you identify the Transaction:

We suggest you maintain Transaction Receipts in chronological order so that you can retrieve them quickly and easily when needed. Records may be stored off site, provided they are secure and readily accessible to the appropriate personnel. Remember, all records must be retained for a minimum of two (2) years.

Your response to a Retrieval Request may be sent by U.S. mail, Autofax or online, as outlined in the Retrieval Request notice. Due to possible delays using U.S. mail, we recommend that you submit your response via Autofax, online or send it via overnight mail. If you elect to send your response via U.S. mail, make sure you allow sufficient time to meet the deadline.

If we do not receive your response to the Retrieval Request by the deadline given, a Chargeback will be issued and your DDA will be debited for the amount of the Transaction. This type of Chargeback cannot be reversed. To avoid such Chargebacks, you should make it a priority to respond to Retrieval Request notices as soon as you receive them.

A Chargeback is a Transaction disputed by the Cardholder or an Issuer. If you receive a Chargeback, we debit your DDA for the amount of the Transaction, including any applicable currency fluctuations, and send you a Chargeback notice. This notice includes the details of the Transaction as well as specific instructions on how to respond.

There are several situations in which Chargebacks may occur. The most common Cardholder-initiated disputes include:

While it may not be possible to eliminate Chargebacks entirely, you can reduce their occurrence by resolving issues and disputes directly with the Cardholder and by following the proper Authorization and processing procedures. Because Chargebacks can be costly to the Merchant, you should make every effort to prevent them. Generally, you should remember to:

A Merchant’s written reply to a Chargeback is known as a Chargeback rebuttal.

You must submit your rebuttal to us in a timely manner so we can present it to the Issuer. If you submit a valid rebuttal, we issue a provisional credit in the amount of the Transaction to your DDA. The Issuer will then review your rebuttal to determine if the Chargeback is remedied. If the Issuer determines that the Chargeback is not remedied, they will initiate a second Chargeback and we debit your DDA a second time.

You must submit a legible and valid rebuttal within the time frame specified in the Chargeback notice. Failure to do so will delay credit to your DDA and may result in a waiver of your right to rebut the Chargeback.

For more information on rebuttal procedures, contact the Chargeback department using the toll free number provided in the Chargeback Notice.

There are specific instances when a Chargeback cannot be reversed. In these cases, you are responsible to us for the Transaction amount regardless of the Authorization Code you received. These situations include:

Merchant’s presentation to Servicer of Excessive Activity will be a breach of the Agreement and cause for termination of the Agreement if the Excessive Activity thresholds outlined in this section are met for Merchant’s accounts as a whole. Alternatively, in Servicer’s sole reasonable discretion, if Excessive Activity occurs for any one or more POS Device identification number(s) or MID(s), only the account(s) that meet the Excessive Activity threshold may be terminated. “Excessive Activity” means, during any monthly period, Chargebacks and/or Retrieval Requests in excess of one percent (1%) of the gross dollar amount of Merchant’s Transactions or returns in excess of two and one-half percent (2.5%) of the gross dollar amount of Transactions. Merchant authorizes, upon the occurrence of Excessive Activity, Member and Servicer to take additional actions as either of them may deem necessary including, without limitation, suspension of processing privileges or creation or maintenance of a Reserve Account in accordance with the Agreement.

Chapter 7

Dynamic Currency Conversion (DCC) is a service that allows a Merchant to offer international Cardholders the option to pay in their home currency rather than U.S. Dollars at the point-of-sale. The following describes how to process Dynamic Currency Conversion Transactions for the designated Cards. These guidelines can help you:

You must register with the Payment Networks through us prior to offering DCC service to Cardholders. You have sole responsibility to comply with Laws and Payment Network Regulations governing DCC Transactions, including all of the following:

You must comply with the following DCC Cardholder written disclosure requirements in all acceptance environments, with the exception of telephone order (TO) Transactions.

For TO Transactions, you must verbally notify the Cardholder of all the disclosure requirements listed above before initiating a DCC Transaction.

In addition to the appropriate electronic or manual Transaction Receipt requirements, DCC Transaction Receipts must also include:

Prior to initiating an MO DCC Transaction, you must ensure that the following information is included on the MO form:

Prior to initiating an Electronic-Commerce (EC) DCC Transaction, you must inform the Cardholder of all of the DCC Written Disclosure Requirements listed above. You must provide this information with an “accept” or other affirmative button that requires Cardholder agreement to proceed.

Prior to initiating a T&E DCC Transaction, you must inform the Cardholder of all of the following information:

This information must be documented in a written agreement that is signed by the Cardholder before checkout or rental return that authorizes Merchant to deposit a Transaction Receipt without the Cardholder’s signature for the total amount of their obligation. Further, the Cardholder must expressly agree to DCC by marking the “accept” box on the written agreement.

The Merchant must send the Cardholder a copy of the Transaction Receipt through the postal service (or by email if selected by the Cardholder) within three (3) business days of completing the Transaction.

Multi-Currency Pricing (MCP) is a service that allows a Merchant to display the price of goods or services in a currency other than, or in addition to, your local currency. You have sole responsibility to comply with Laws and Payment Network Regulations governing MCP, including all of the following:

In addition to the appropriate electronic or manual Transaction Receipt requirements, it is important that the Transaction Receipt clearly shows the Transaction currency and the corresponding currency symbol or code. The currency code is the three digit ISO alpha country code. For Transaction Receipts without a currency symbol or code, the receipt will be assumed to be in Merchant’s local currency, which may give rise to rights of Chargeback.

Chapter 8

In addition to the Authorization procedures set out in this document, Merchants that provide vehicle rental shall follow the procedures set out in this Chapter.

You must prepare Transaction Receipts for all Transactions as described in Chapter 2, Transaction Receipts. The Cardholder must sign the Transaction Receipt. However, the Cardholder must not be required to sign until the total Transaction amount is known and indicated on the Transaction Receipt.

The Merchant will include all items of goods and services purchased or leased in a single Transaction in the total amount of a single Transaction Receipt except:

If Merchant is engaged in vehicle rental or leasing, Merchant may obtain Authorization for such Transactions based upon estimates of the Transactions according to the following procedures:

1. The Merchant estimates the amount of the Transaction based on the Cardholder’s intended rental period at the time of rental, the rental rate, tax and mileage rates and ancillary charges. The estimate may not include an extra amount for possible car damage, or for the insurance deductible amount if the Cardholder has waived insurance coverage at the time of rental.

2. If the Merchant later estimates that the Transaction amount will exceed the initial estimated Transaction amount, the Merchant may obtain additional authorizations for additional amounts (not cumulative of previous amounts) at any time before the rental return date. The Merchant must disclose to the Cardholder the authorized amount for the estimated car rental or leasing Transaction on the rental date. A final or additional authorization is not necessary if the actual Transaction amount does not exceed 115% of the sum of the authorized amounts.

3. If the Merchant alters a Transaction Receipt or prepares an additional Transaction Receipt to add delayed or add-on charges previously specifically consented to by the Cardholder, the Merchant must deliver an explanation of the change to the Cardholder (i.e., mail a copy of the amended or additional Transaction Receipt to the Cardholder), and the Merchant must fully comply with the requirements in Chapter 8, Vehicle Rental Or Leasing Ancillary Charges.

4. Regardless of the terms and conditions of any written pre-Authorization form, the Transaction Receipt amount for a vehicle rental or lease Transaction cannot include any consequential charges. The Merchant may pursue consequential charges set forth in its terms and conditions by means other than Card Transaction.

If the Merchant discovers additional ancillary charges or an error in calculation after the rental car is returned, the Merchant may bill the Cardholder provided that the signed rental contract allows for additional charges and final audit.

The Merchant may not recover charges related to car damage, theft or loss. Valid charges may include:

Parking tickets and other traffic violations For parking tickets and traffic violations:

These charges must be processed on a delayed or amended Transaction Receipt within 90 calendar days of the rental return or base end date. A copy of this Transaction Receipt must be mailed to the Cardholder’s address as indicated in the rental contract or folio. This Transaction Receipt does not require the Cardholder’s signature if the Merchant:

Chapter 9

In addition to the Authorization procedures set out in this document, Merchants that provide lodging accommodations in the hotel and hospitality industry shall follow the procedures set out in this Chapter.

You must prepare Transaction Receipts for all transactions as described in Chapter 2, Transaction Receipts. The Cardholder must sign the Transaction Receipt. However, the Cardholder must not be required to sign until the total Transaction amount is known and indicated on the Transaction Receipt.

The Merchant must include all goods and services purchased or leased in a single Transaction in the total amount of a single Card Transaction except:

The Merchant may obtain authorizations for Card Transactions involving the provision of lodging accommodations based upon estimates of the transactions according to the following procedures:

1. The Merchant must estimate the amount of the Transaction based on the Cardholder’s intended length of stay at check-in time, the room rate, applicable tax and/or service charge and any Merchant-specific methods for estimating additional ancillary charges. Merchant must request Authorization for the estimated amount of the Transaction.